At its peak, Ethiopia was widely described by international financial institutions as one of Africa’s most promising frontier investment destinations. Between 2010 and 2019, Ethiopia was widely regarded as a frontier investment success story. According to the World Bank and IMF macroeconomic datasets, the country recorded average GDP growth of around 9% annually during the decade before COVID-19, driven largely by state-led infrastructure expansion and rising foreign direct investment (FDI).

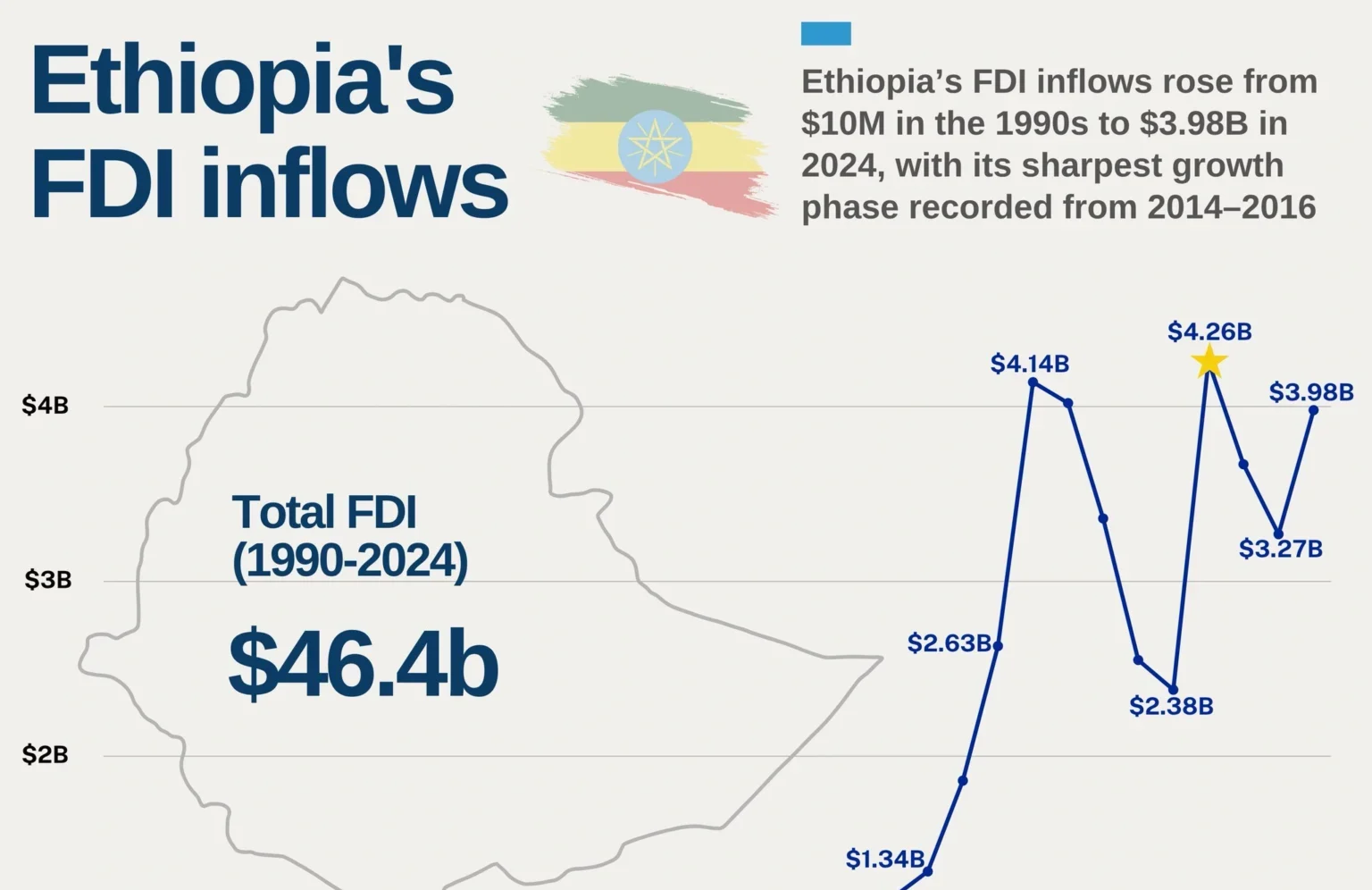

Between 2010 and 2019, the country experienced one of the fastest expansions of foreign direct investment (FDI) in Sub-Saharan Africa, driven by state-led industrialisation, infrastructure megaprojects, and manufacturing zones. According to the World Bank’s development indicators, Ethiopia’s FDI inflows rose from less than $1.1 billion in 2010/11 to over $4 billion by 2016/17, marking one of the steepest investment growth curves in Africa during that period.

By 2021, inflows reached approximately $3.9 billion, partly boosted by Ethiopia’s telecom liberalisation and the entry of Safaricom into the market. The UNCTAD World Investment Report 2023 further confirms Ethiopia’s position as a key investment hub in East Africa, recording $3.7 billion FDI inflows in 2022, though already showing a downward trend from previous years.

Yet beneath this upward trajectory, a structural vulnerability was forming, one that would become visible after 2020.

The Conflict Turning Point: 2020 and the Repricing of Risk

The outbreak of the Tigray conflict in 2020, followed by continued instability in parts of Amhara and Oromia, fundamentally altered investor risk calculations. The 2022 Center for International Private Enterprise (CIPE) assessment shows that real sectors of the economy have been significantly affected by the conflict. Medium, Small, and Micro-Sized Enterprises (MSMEs) operators in all regions have informed us that they have either reduced their operations significantly (by 60-80%) or shut their businesses down.

A 2024 macroeconomic profile of Ethiopia notes that FDI inflows dropped during periods of instability, particularly where industrial parks and transport corridors were affected by insecurity and logistical disruption.

Satellite-based research on conflict-affected regions of Ethiopia shows that even when agricultural production remained resilient, broader economic systems, including logistics and market access, were heavily disrupted during conflict periods.

An investment analyst, Mesfin Menza, quoted in a World Bank–linked policy review summarized the shift bluntly:“ Conflict risk is not only about destruction, it is about repricing the entire investment environment, from insurance premiums to supply chain predictability.”

Industrial Parks under Pressure

Ethiopia’s industrial parks; once marketed as engines of export-led growth became a central indicator of this shift. The Hawassa Industrial Park, one of Africa’s flagship textile export zones, faced factory closures and job losses after Ethiopia lost preferential access to the U.S. market under the African Growth and Opportunity (AGOA) restrictions linked to the conflict. At its peak, the park employed more than 35,000 workers, but experienced significant disruptions during 2022–2023 due to market access restrictions and investor withdrawal pressures.

Consistent with this, Ethiopia experienced significant economic setbacks following the suspension of AGOA in January 2022, according to the African Development Bank Group’s (AfDB) Country Focus Report 2025. The report highlights that Ethiopia’s manufacturing economy has taken a significant hit since its suspension from AGOA.

The World Bank’s industrialisation assessment report highlights that Ethiopia’s industrial model is highly sensitive to external shocks, particularly those affecting export logistics and political instability.

A factory supervisor at an industrial zone in Oromia Mrs Alemitu (name withheld for safety reasons) described the operational reality as: “We can produce. But uncertainty kills contracts. Buyers don’t wait when there is conflict risk.”

FDI Trend Disruption: Data Signal of Instability

While Ethiopia maintained relatively strong FDI inflows compared to regional peers, the UN Trade and Development (UNCTAD) and UNIDO trend shows volatility:2016/17: ~ $4.1 billion peak growth phase, 2019/20: ~ $2.4 billion decline due to instability and COVID-19 shocks, 2021: rebound to ~$3.9 billion, 2022: decline to ~$3.7 billion.

The UNCTAD World Investment Report confirms that global FDI fell by 12% in 2022, but stresses that instability disproportionately affects fragile economies already dependent on external financing.

According to UNCTAD/World Bank data Ethiopia’s FDI inflows peaked at more than $4 billion in 2016–2017, declined to about $2.4–2.5 billion by 2019–2020, and later recovered to nearly $4 billion in 2024.

The Ethiopian Investment Commission also reported FDI inflows of approximately $3.82 billion during the 2023/24 Ethiopian fiscal year, consistent with the UNCTAD trend.

While there are signs of slow recovery in 2025 and 2026, with inflows rising slightly, the overall trend paints a grim picture.

Despite the marginal increase in capital inflows, Ethiopia still grapples with the FDI challenges due to the ongoing regional conflict and unstable political environment.

A senior African development economist, Pierre Nguimkeu, Director of the Africa Growth Initiative (quoted in a Brookings-style policy briefing) noted:“ FDI does not disappear in conflict economies; it becomes selective, risk-sensitive, and concentrated in extractive or highly secured sectors.”

From Growth Narrative to Risk Narrative

Before 2020, Ethiopia’s investment story was driven by: Industrial parks expansion, Infrastructure megaprojects, Chinese-financed railways and energy systems, Liberalisation of telecom and logistics.

After 2020, the narrative shifted to security risk premiums, currency shortages, contract uncertainty and Investor hesitancy.

A policy analysis by international development institutions notes that Ethiopia’s investment performance remains structurally strong but increasingly constrained by non-economic risks, including governance and conflict exposure.

The Emerging Pattern: Investment under Political Stress

Across Africa, research by UNCTAD and development agencies shows that: countries experiencing conflict see longer FDI recovery cycles, Infrastructure and manufacturing FDI are the most sensitive to instability. Investors increasingly prefer “politically insulated” sectors such as digital services or extractives. Ethiopia now reflects this broader continental trend where investment inflows continue, but confidence becomes uneven.

- Capital under Fire: Industrial Parks, Debt Pressures, and the Hidden Mechanics of “Corrosive Capital” in Ethiopia

At the edge of Hawassa Industrial Park, sewing machines hum in long warehouse halls where thousands of young workers stitch garments destined for Europe and the United States. Outside the gates, buses arrive before sunrise carrying mostly young women from surrounding rural towns.

For many workers, this is the promise of Ethiopia’s industrial transformation. For others, it is also where the debate over FDI becomes most visible in everyday life.

Ethiopia’s industrial park strategy, launched in the mid-2010swas designed to shift the country from an agrarian economy into a manufacturing hub. The World Bank and government planners positioned it as a flagship export-led growth model. But nearly a decade later, Yohannes Ayele and Sherillyn Raga, Senior Research Officers at ODI, explain that the model now sits at the intersection of job creation, debt exposure, and what governance scholars describe as “corrosive capital” dynamics: investment flows that generate growth but may weaken long-term sovereignty, transparency, and local value capture.

- Industrial Parks: Growth Engine or Low-Wage Dependency Model?

Hawassa Industrial Park is often cited as Ethiopia’s most advanced eco-industrial zone. According to the Industrial Parks Development Corporation (IPDC), the park hosts more than 20 foreign firms and has created tens of thousands of jobs, mainly in textiles and garments.

In official framing, industrial parks are a success story: export earnings, industrialisation, and foreign exchange generation.

But independent assessments suggest a more complex picture.

A 2023 UNDP economic review notes that Ethiopia’s manufacturing sector remains “weak relative to services growth,” despite years of industrial park expansion and foreign investment inflows.

Workers interviewed in multiple reports describe wages that often range between 3,000–5,000 ETB (20-25 USD) per month, alongside high turnover rates and limited long-term job security.

A former factory supervisor Mr. Awoke (name withheld for security reasons) described the situation as follows:

“The jobs are real, but the pressure is constant. Many workers leave within months because the wages do not match the cost of living or the workload expectations.”

Labour experts argue that this reflects a structural feature of export-led industrial parks in low-income economies: competitiveness is often built on low labour costs rather than productivity gains or domestic supply-chain integration.

A governance researcher at an East African Policy Institute (anonymous due to sensitivity of ongoing research) explained:

“Industrial parks can become either stepping stones for industrial upgrading or locked systems of dependency. The difference depends on local ownership, wage growth, and technology transfer.”

- Debt and Development Financing: The Infrastructure Trade-Off

Ethiopia’s industrialisation strategy is tightly linked to external financing. Alongside industrial parks, large infrastructure projects, including railways, energy systems, and logistics corridors have been financed heavily through external loans.

According to UNCTAD’s World Investment Report, Ethiopia remained among the top recipients of FDI in Least Developed Countries, receiving around $3.7 billion in 2022, despite a decline from previous years.

However, the same period also saw rising debt vulnerability concerns.

The IMF has repeatedly flagged Ethiopia as facing serious external debt distress risks, particularly due to foreign currency shortages and repayment pressure under restructuring negotiations.

A 2024 UNDP economic profile further highlighted that: foreign reserves fell below critical import coverage thresholds, inflation remained above 25% in multiple periods, debt servicing increasingly competed with social spending priorities.

Woretaw Motbaynor, an economist specializing in African infrastructure finance (quoted in a regional development forum report), noted:

“Debt-financed infrastructure is not inherently problematic. The issue is whether the returns economic and fiscal are sufficient to service the obligations without crowding out essential domestic investment.”

The following graph illustrates the debt exposure in Ethiopia and how this debt weakens FDI.

This is where analysts identify one dimension of corrosive capital risk: when infrastructure financing becomes structurally dependent on foreign-currency revenue streams that are weaker than repayment obligations.

Mechanisms of Corrosive Capital in Industrial Development

Based on interviews with policy analysts, four recurring mechanisms emerge in Ethiopia’s industrial park and infrastructure model. These are:

- Export Dependency without Domestic Integration

Most industrial park output is export-oriented, with limited local supply-chain linkages. Inputs are often imported, reducing domestic multiplier effects.

- Foreign Currency Pressure

Revenue is often earned in foreign currency, while operational costs and debt repayment also depend on external currency availability. Ethiopia’s chronic forex shortages intensify this imbalance.

- Technology and Management Concentration

Many parks rely on foreign firms for management systems, quality control, and logistics coordination. This limits rapid localisation of technical expertise.

- Land and Incentive Structures

Long-term land leases and tax incentives attract investors but reduce immediate fiscal returns for the state.

Mr Degye Goshu, Director of Research and Policy Analysis, Ethiopian Economics Association (EEA),a development policy researcher summarized this model as:

“It is not exploitation in a classical sense. It is structural dependence created by the architecture of financing and production.”

Human Stories: Between Opportunity and Constraint

Inside Hawassa Industrial Park, workers describe mixed realities.

A 24-year-old machine operator Abreham (name changed) said:

“I send money home every month. But I still feel like I am always behind. If I stop working, I cannot survive.”

Others describe the psychological pressure of high production quotas and repetitive work.

At the same time, employers and policymakers highlight gains: formal employment, export earnings, and skills exposure.

A factory manager,Ms Tsga Hailu, noted:

“For many workers, this is their first formal job. It changes their economic mobility, even if challenges remain.”

This duality reflects a broader tension in Ethiopia’s development model: rapid job creation versus structural transformation.

Debt, Industry, and the Governance Question

Industrial parks cannot be separated from Ethiopia’s wider debt-financed development strategy. The Addis Ababa–Djibouti corridor, energy expansion projects, and industrial zones are all interconnected through external financing ecosystems.

UNCTAD data shows that developing countries face a growing investment gap in achieving sustainable development goals, estimated at trillions of dollars annually.

In this context, Ethiopia’s strategy reflects a global pattern: infrastructure-led growth financed by external capital.

But governance experts caution that the key variable is not capital inflow, but contract transparency, debt sustainability, and institutional capacity.

Constructive vs. Corrosive Capital: the Policy Divide

In policy discussions, CIPE analysis increasingly distinguishes between: Constructive capital investment that builds local capacity, enhances transparency, and strengthens institutions. And corrosive capital investment that may generate growth but increases dependency, opacity, or long-term vulnerability

As one regional governance analyst summarized:

“The question is not whether Ethiopia needs foreign capital. The question is under what conditions that capital supports sovereignty rather than undermining it.”

A System under Pressure

Industrial parks remain central to Ethiopia’s ambition to become a manufacturing hub. Yet they now operate in an environment shaped by:foreign exchange shortages, debt restructuring negotiations, global supply chain volatility, and regional security instability.

The result is a development model under continuous negotiation between growth and constraint.

In Addis Ababa’s policy circles, the debate over foreign investment has become increasingly polarized.

To government officials, Ethiopia remains one of Africa’s most strategic investment destinations, with reforms aimed at opening telecoms, banking, logistics, and manufacturing to global capital.

To critics, however, the same investment architecture, especially in infrastructure, industrial parks, and digital systems, reflects a deeper structural vulnerability: a development model exposed to debt pressure, conflict shocks, and what some governance analysts describe as corrosive capital dynamics.

Between these two narratives sits a more uncertain reality: investors adjusting quietly to risk, workers navigating instability, and policymakers trying to maintain growth momentum under constrained conditions.

Political Narratives: Reform, Resilience, and Risk

Government officials consistently frame Ethiopia’s investment climate as one of long-term opportunity.

Dr. Brook Taye, chief executive officer of Ethiopian investment holdings(public statements and policy briefings) has repeatedly emphasized that industrialisation and infrastructure expansion remain central to national transformation, even under challenging conditions.

In official investment messaging, he said Ethiopia is still presented as: a gateway to the Horn of Africa market, a large labour pool economy, a strategic logistics corridor economy and a reform-oriented investment destination.

At the same time, policy documents from institutions such as the World Bank and IMF acknowledge persistent macroeconomic pressures, including foreign currency shortages and debt sustainability challenges.

The Investor Perspective: Confidence under Pressure

Foreign investors operating in Ethiopia describe a more cautious environment than in the pre-2020 period. Wim Vanhelleputte, CEO at Safaricom Ethiopia; Alex Song CEO, GOBEZ Electric Manufacturing PLC; Ben Depraetere, Managing Director Nunhems; Kishen Raval, Managing Director at Habesha Steel Mills PLC and Zhang Huarong CEO at Huajian Group, in a panel discussion, stated that across industrial parks, logistics companies, and manufacturing zones, common concerns include security disruptions in conflict-affected regions, supply chain unpredictability, foreign exchange limitations, insurance and risk premiums and regulatory uncertainty during transitions.

A European manufacturing investor operating in an industrial park Mr Johnston (name withheld due to commercial sensitivity) said:

“The fundamentals are still attractive, but risk calculations have changed significantly. Stability matters as much as cost.”

A regional trade analyst from a multilateral development institution noted:

“Investment decisions in fragile contexts are increasingly driven by risk pricing rather than opportunity alone.”

These shifts reflect broader global trends identified in UNCTAD’s World Investment Report, which documents volatility in FDI flows to developing economies during periods of political uncertainty.

Conflict and the Investment Climate Shock

Since 2020, Ethiopia has experienced overlapping security challenges across multiple regions, including Tigray, Amhara, and Oromia.

International reporting by agencies such as Reuters and other global financial media has repeatedly linked political instability to investor caution, supply chain disruptions, and delayed investment decisions in manufacturing and infrastructure sectors.

While Ethiopia remains a significant recipient of foreign capital, analysts note that: project timelines have slowed, some investors have paused expansion plans, risk insurance premiums have increased and long-term capital commitments have become more selective

A governance researcher specializing in African Political Economy, Amare Matebu, observed:

“Conflict does not always stop investment, but it changes its structure. Investors become more short-term, more risk-averse, and more extractive in behavior.”

The debate over foreign investment in Ethiopia is not purely economic, it is deeply political.

Mr Ahmed Shedie argues that: foreign capital is essential for infrastructure gaps, industrial parks create jobs and export revenue, telecom and energy investments modernise the economy, and debt-financed development is a necessary stage of growth.

A senior policymaker, Hana Tehelku (public remarks in economic forums),emphasized that:

“No country has industrialized without external capital. The issue is not borrowing; it is how borrowing is managed.”

Opposition figures, independent economists, and civil society voices argue differently.

An opposition economist and political commentator ,Mr. Mushe Semu, warned:

“When debt-financed projects are concentrated in foreign-controlled systems without sufficient transparency, the risk is not just economic, it becomes political and structural.”

Critics argue that:debt obligations reduce fiscal flexibility, opaque contracts limit accountability, external dependence shapes policy spaceand local industries may remain weakly integrated.

This framing aligns with governance research on corrosive capital, where investment is not necessarily harmful in intent but may produce long-term dependency effects due to structure and governance conditions.

Ethiopia’s Investment Model: Growth with Constraints

Ethiopia’s development model over the past decade has combined: state-led infrastructure expansion, foreign-financed mega-projects, industrial park-led manufacturing strategy and rapid digital transformation.

This model has produced visible outcomes: roads, railways, factories, and telecom expansion.

But it has also generated structural tensions identified by Tale Geddafa analysis: debt sustainability challenges, foreign currency shortages, uneven domestic value addition and dependency on external technical systems.

A development economist summarized it as:

“Ethiopia’s model is neither a failure nor a full success. It is a transition system under stress.”

The Bigger Question: What Kind of Capital Builds Sovereignty?

Across all sectors examined, railways, industrial parks, telecom systems, and conflict-affected investment flows, central question emerges: What distinguishes constructive capital from corrosive capital in practice?

From CIPE literature and development research, key distinguishing factors include: transparency of contracts, local ownership and capacity transfer, debt sustainability, institutional strengthening, and long-term economic autonomy.

Where these are weak, investment may still generate growth, but with increasing structural dependency risks.

Conclusion

Ethiopia stands at a critical intersection of development ambition and structural constraint.

Foreign investment remains essential to its economic transformation. Yet the form that investment takes, its transparency, its financing structure, its technological ownership, and its political economy will determine whether it strengthens or constrains long-term sovereignty.

READ ALSO: NACA, Global Fund and Partners to convene national close-out meeting on COVID-19 response mechanism investments in Nigeria

As Degye Goshu, an Ethiopian policy analyst, summarized:

“Capital does not arrive neutral. It arrives with architecture, conditions, and consequences.”

The story of Ethiopia’s foreign investment is therefore not only about railways, factories, or telecom networks.

It is about the architecture of development itself and who ultimately controls it.

Acknowledgement

This story was supported by the Centre for Journalism Innovation and Development (CJID) with funding support from the Center for International Private Enterprise (CIPE).